How did they do? Ukrainian agroholdings' performance

2011-05-05 11:42:33

Now that the government is getting ready to drop export quotas and tax exports directly, we have had some time to look company performance. Also the 2010 reporting year is almost complete and we expect Astarta and Sintal to be coming out shortly.

However we went ahead and will later update company performance. In 2009 we saw the following picture:

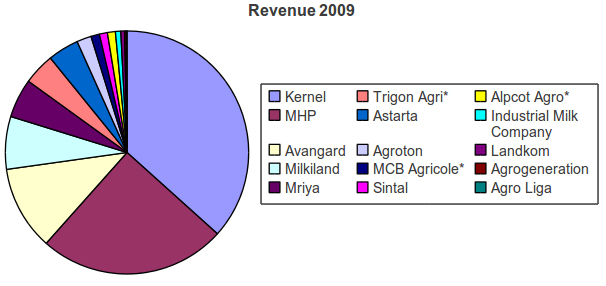

| 2009 | |||

| COMPANY | Revenue | Ebitda | EBITDA % |

| Kernel | $1 047 100 000 | $190 000 000 | 18% |

| MHP | $711 000 000 | $271 000 000 | 38% |

| Avangard | $320 000 000 | $152 000 000 | 48% |

| Milkiland | $200 008 000 | $32 460 000 | 16% |

| Mriya | $148 349 000 | $98 700 000 | 67% |

| Trigon Agri* | $119 593 616 | -$11 391 120 | -10% |

| Astarta | $117 718 000 | $50 085 000 | 43% |

| Agroton | $55 300 000 | $21 200 000 | 38% |

| MCB Agricole* | $32 328 000 | $3 112 000 | 10% |

| Sintal | $30 432 000 | $9 951 000 | 33% |

| Alpcot Agro* | $30 165 480 | -$53 561 800 | -178% |

| Industrial Milk Company | $20 206 000 | $8 410 000 | 42% |

| Landkom | $14 553 000 | -$27 445 000 | -189% |

| Agrogeneration | $5 987 640 | na | |

| Agro Liga | $2 767 458 | na | |

| $2 855 508 194 | $744 520 080 | 26% | |

In 2009 Ukrainian public agricultural companies earned a little less than $3 billion and had on average an EBITDA of 26%. This was at a time when commodity markets were quiet.

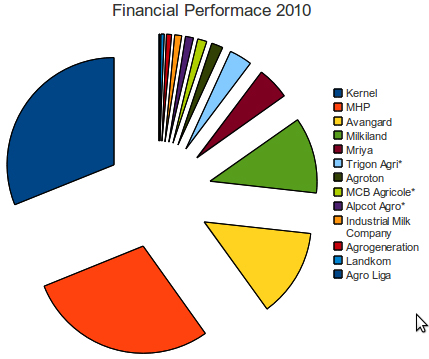

The picture in 2010 should be better because prices have improved. On the down side was the export quota's which should have bitten into revenues. Our analytical team has learned long ago that Ukraine's farmers, regardless of their size will never get full returns when market improve. The picture was as as follows:

| 2010 | |||

| COMPANY | Revenue | Ebitda | EBITDA % |

| Astarta | na | na | |

| Sintal | na | na | |

| Kernel | $1 020 500 000 | $190 000 000 | 19% |

| MHP | $944 000 000 | $325 000 000 | 34% |

| Avangard | $440 000 000 | $194 000 000 | 44% |

| Milkiland | $377 513 400 | $64 177 278 | 17% |

| Mriya | $161 524 000 | $152 765 000 | 95% |

| Trigon Agri* | $113 289 070 | $2 044 560 | 2% |

| Agroton | $57 300 000 | $35 100 000 | 61% |

| MCB Agricole* | $46 000 000 | $6 200 000 | 13% |

| Alpcot Agro* | $39 563 440 | -$22 377 660 | -57% |

| Industrial Milk Company | $34 800 000 | $19 500 000 | 56% |

| Agrogeneration | $25 410 960 | na | |

| Landkom | $16 799 000 | -$11 698 000 | -70% |

| Agro Liga | $5 543 678 | na | |

| TOTAL | $3 282 243 548 | $954 711 178 | 29% |

In total we expect revenue will increase to over $3,5 billion and EBITDA will also improve. Another way of reading these results is to speculate what would happen if all of Ukraine's farmland was farmed in the same way as the agro holdings. The agro holdings listed above control and farm 1,400,000 hectares of land, meaning they realize $2,344 of revenue per hectare. If all of Ukraine's 35 million hectares was farmed in the same manner it would lead to agricultural production of $82 billion. If we added value added processing it would lead to triple the revenues or $246 billion annually. That would be twice the current GDP. Think about it.